The BIG Untapped Asset -- Confidence

Don’t underestimate the power of something we have not yet witnessed in this recovery/Bull market cycle – the potential emergence of “Animal Spirits”!

The economy and the stock market are driven by several factors – interest rates, monetary and fiscal policies, the inflation rate, productivity, job creation, and profitability – to name just a few. But probably one of the biggest factors, and often overlooked, is private sector confidence. Nobody starts a new company, expands existing operations, adds staff, quits a job for a better perceived opportunity, or buys a new house without optimism and confidence in the future! Indeed, when pessimism rules and grips the psyche of economic players, little else matters. Once the private sector becomes severely depressed and petrified, even massive fiscal juice, negative interest rates, and a mountain of money supply will struggle in reviving the economy. Similarly, when Main Street becomes irrationally exuberant, as the maestro Alan Greenspan experienced, it can prove equally daunting to moderate with conventional economic tools.

Given its importance, it’s rather surprising how little attention confidence receives. After all, the U.S. has a fiscal authority who can tax and spend, a Federal Reserve overseeing the financial industry and controlling the money supply, a body in charge of setting the short-term interest rate, a Labor Bureau, a Business Bureau, and a Consumer protection agency, but no “Confidence Czar”. I guess you could argue the media – both conventional and online – greatly impacts confidence but given their focus on eyeballs and clicks, they commonly play the role of a Pessimism Czar.

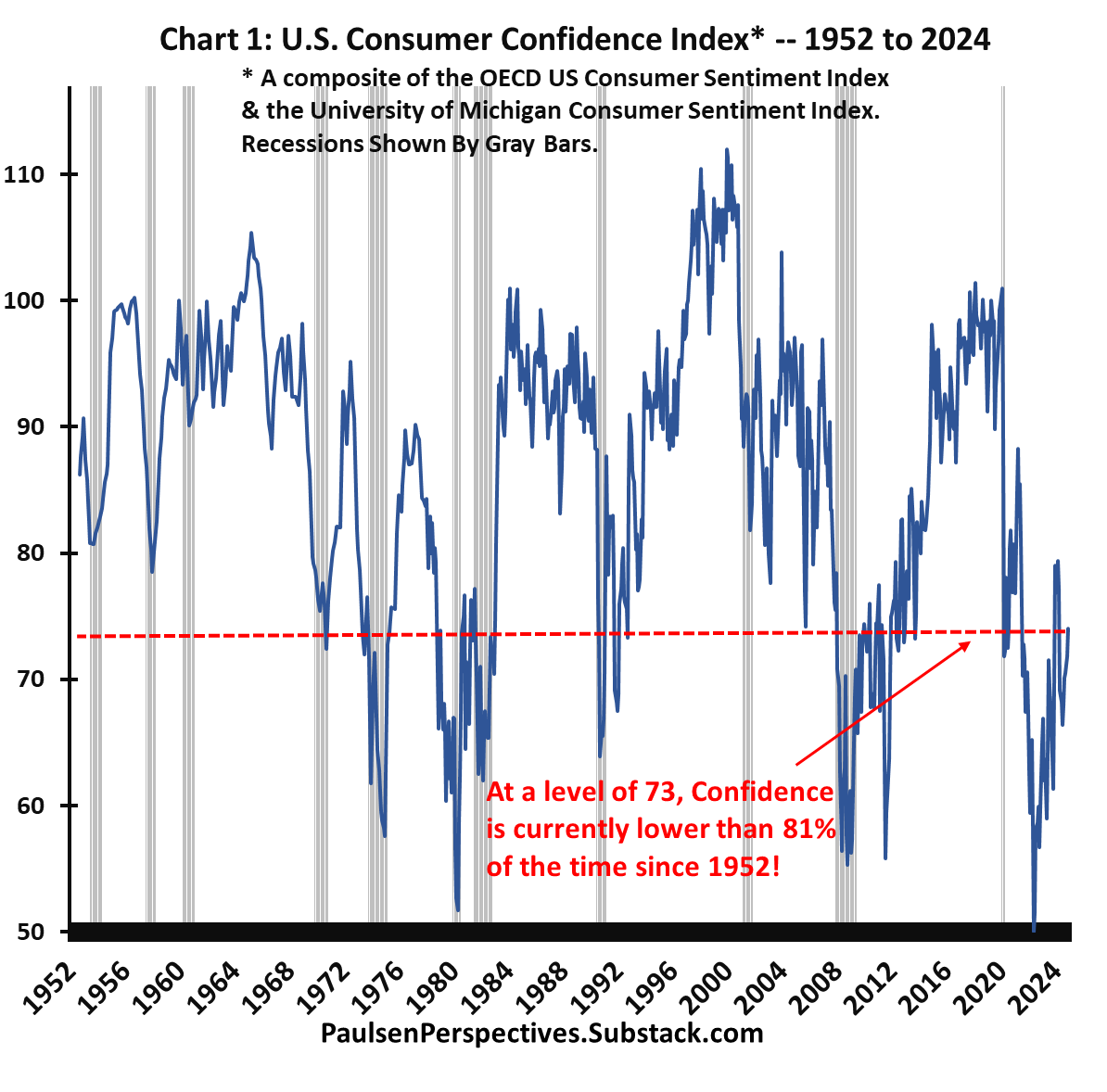

Main Street confidence is a dominant factor in every economic expansion but has proved particularly meaningful in the cotemporary recovery. Normally, as demonstrated in chart 1, confidence collapses during recessions and then revives once a new economic expansion begins. However, since the 2020 pandemic recession, U.S. confidence has never really recovered. After more than four years since the last recession and over two years since the last Bear market, Main Street confidence remains lower than 81% of the time since 1952. Unique to the post-war era, the post-pandemic economic expansion and its corollary Bull market have yet to revive U.S. confidence.

This is unfortunate because confidence may be the biggest economic & Bull market weapon in the arsenal. Typically, the degree of improvement in Main Street confidence plays a huge role in the success of the economic cycle and the size of returns for equity investors. But fortunately, since this asset has not yet been tapped, if something or someone could boost U.S. cultural sentiment, both the performance of the economy and the current stock market run could be elongated and enhanced. Traditionally, four years into an economic recovery, Main Street confidence would already be near historic highs, leaving little room for improvement. Normally at this point, excessively strong confidence among private sector players (exhibiting overly exuberant private player risky behaviors) would represent a recession and bear market risk. Instead, today, because Main Street confidence remains conservative and pessimistic those risks remain surprisingly low.

Consequently, the rest of this economic expansion and its Bull market may depend less on what the Congress, or the Federal Reserve does than on what happens with Main Street confidence. It is worthwhile, therefore, to examine the recent improvements in confidence measures, what factors may continue helping to restore confidence, and what this implies about the future of the economic recovery and its Bull market.

Keep reading with a 7-day free trial

Subscribe to Paulsen Perspectives to keep reading this post and get 7 days of free access to the full post archives.