Thanksgiving Leftovers

Jobless claims lose their signal, bond yields to decline toward 3%, cyclical stocks poised for outperformance, tech stocks invariant to Fed conditions, job market driving the policy bus, and more!

Just a few stale thoughts left over from the long holiday weekend. Reheat for a few minutes at 350, add lots of ketchup, grab a cold beverage, and enjoy! It’s the best I could do after celebrating kids, grandkids, grand puppies, and eating lots of turkey & pies!

How Low Can Bond Yields Go?

Currently, the 10-year bond yield is 3.98%, very close to its lowest level since September 2024. Before the confusion caused by the pandemic in 2020 and by its latent inflationary surge during 2021-22, the 10-year Treasury yield traded mostly between 2% to 3% from 2011 to 2019. The Covid crisis is long over and, in my view, so is the post-pandemic inflation calamity. The pace of real GDP growth is near 2% and the job market has flatlined. As it has since the 2009-10 financial crisis, the U.S. economy is still struggling with a slow-growing and aging population, widespread pessimism, and a culture which utilizes much less balance sheet leverage and more conservative cash holdings. With the latest crisis over and the economy seemingly back to its old form of sluggish growth driven by pessimistic players void of animal spirits, why won’t bond yields also return to their old form?

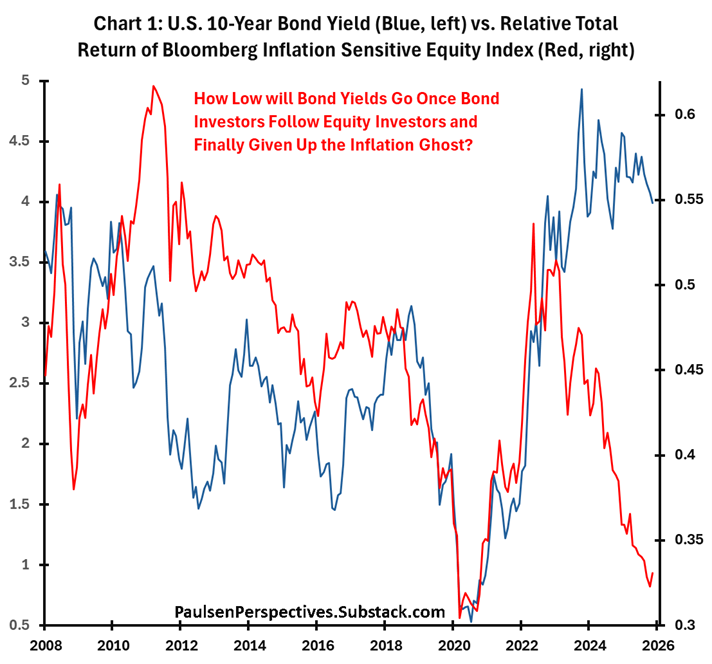

Chart 1 overlays the 10-year Treasury yield with the relative total return of Bloomberg’s inflation sensitive equity index. The Bloomberg Inflation Sensitive Equity Total Return Index is constructed to track the performance of companies with a sector classification of Energy, Industrials, Materials or Real Estate that demonstrate a strong positive correlation with inflation. As shown, equity investors long ago gave up the inflation ghost. The stock market’s most inflation sensitive portions have been underperforming since mid-2022. Prior to the summer of 2022, bond yields moved closely with the relative performance of inflation sensitive equities – that is, both the bond and stock markets were in sync when it came to assessing inflation.

However, since mid-2022, the stock market has moved on from post-pandemic inflation anxieties, but the bond market – perhaps because the Fed keeps fanning fears – has refused to give up the inflation ghost. Recently, though, the Federal Reserve is starting to worry more about real economic growth and appears poised to keep lowering the Fed Funds rate. How low could bond yields finally decline should the Fed and the bond market finally give up the post-pandemic inflation ghost? Could the big story of 2026 be the 10-year bond yield finally catching up with inflation sensitive stocks? Could the 10-year yield surprisingly decline to somewhere between 2.5% to 3% in the coming year as investors’ cultural obsession switches from inflation to real economic growth?