Houston, we have a Problem … Time to Open the Policy Spigot!

Some random thoughts after Friday's Payroll Shocker! Real economic growth at 1%, time for full bull support, companies are lean & mean, correlation suggest a 3% Funds rate, and more ...

From a young age, my kids understood “Payroll Friday”. That was when Dad would either be elated or grumpy! On the first Friday of each month, employment has always been the bellwether for economic reports during the rest of the month. As jobs went, so went the economy.

Frequently, over the years, the jobs numbers “shocked” – by being dramatically better or worse than widely expected and often because of big revisions from past monthly reports. Such was the case for last Friday’s first look at the July economic reports. July nonfarm payrolls only rose by 73,000, nearly 30% below consensus expectations. Even more unsettling, job numbers during the previous two months were revised lower by a shocking 258,000! Only two days earlier, the Federal Reserve assured everyone in its press conference that the job market remained healthy, and they could be patient in deciding when or if to ease monetary conditions. But Friday’s bombshell brought clarity that not only was July a weak month for job creation, but the employment market has been heading south for the last quarter!

Obviously, the President was pretty upset by the report quickly firing the head of the BLS who released the numbers (don’t shoot the messenger Mr. President!). And the Federal Reserve was left quickly rethinking its approach. Houston, we have problem … it’s time to open the policy spigot!

What follows is a quick-hitting pictorial commentary on a series of random indicators which are shaping my thinking. They run the gamut from Fed easing, to a potential recession, to a bear or a bull. Hopefully, you too will find a few of them thought provoking.

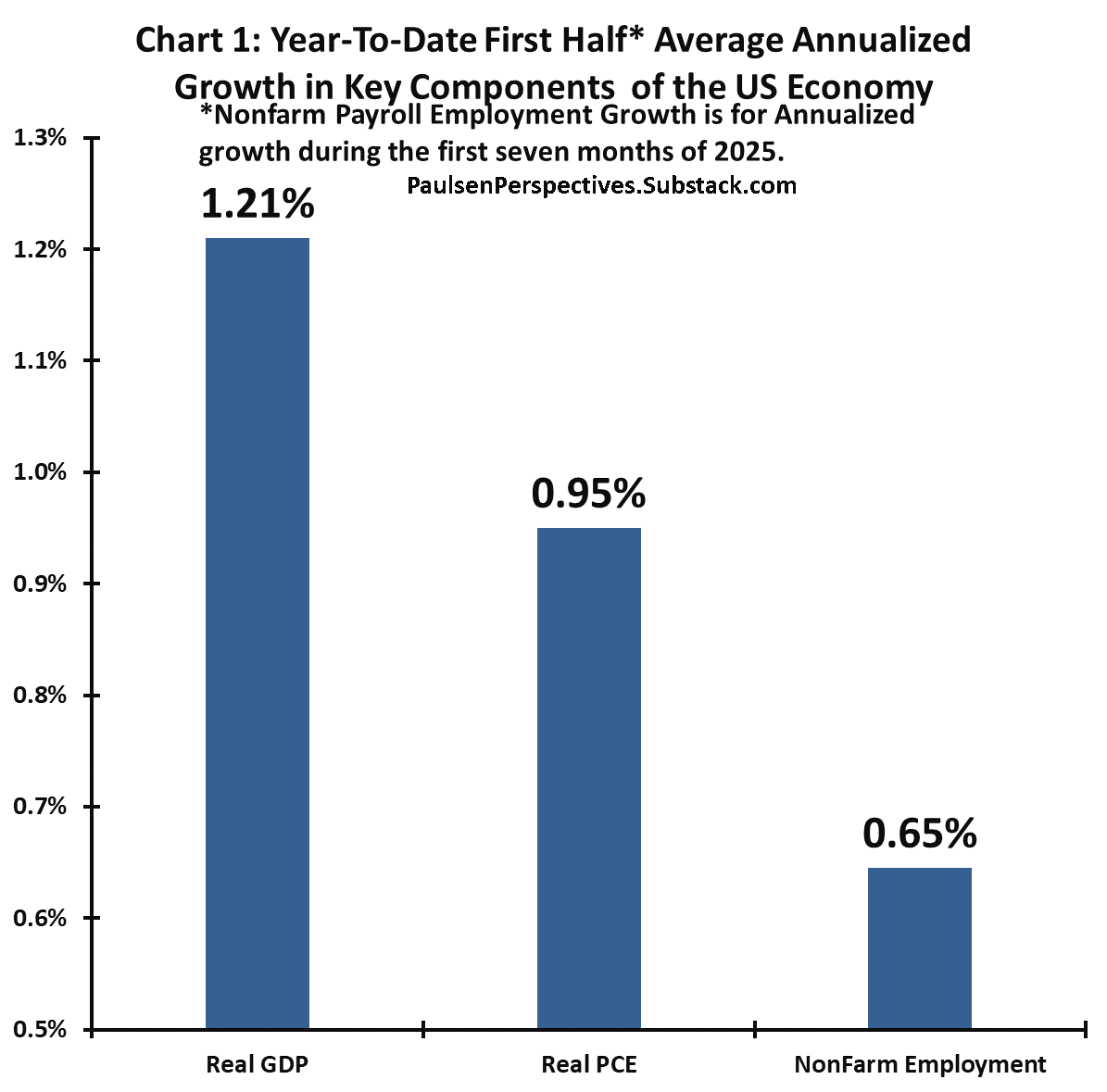

1. Real Economic Growth at 1%?

At its press conference last Wednesday, the Fed kept suggesting the economy was okay and they could afford to be patient. However, as shown in chart 1, real average annualized U.S. economic growth has slowed during the first half of this year to only 1% or less! Real GDP has only risen by 1.2% during the first half while real personal consumption is slightly less than 1%. And with Friday’s job report, nonfarm payroll employment so far this year has risen at an average annualized pace of only 0.65%! Looking at first half growth by averaging the last two quarters eliminates the distortions created in both the first and second quarters by an import surge and then an import collapse as private players were front-running potential tariffs. So, averaging the first half of this year is a pretty good indication of the sustained pace of real U.S. economic growth. What are we doing with a national average 30-year mortgage rate still close to 7% in an economy growing at 1%? There is nothing “healthy or solid” about these numbers, they are way below the 2% stall speed, and shout for help.

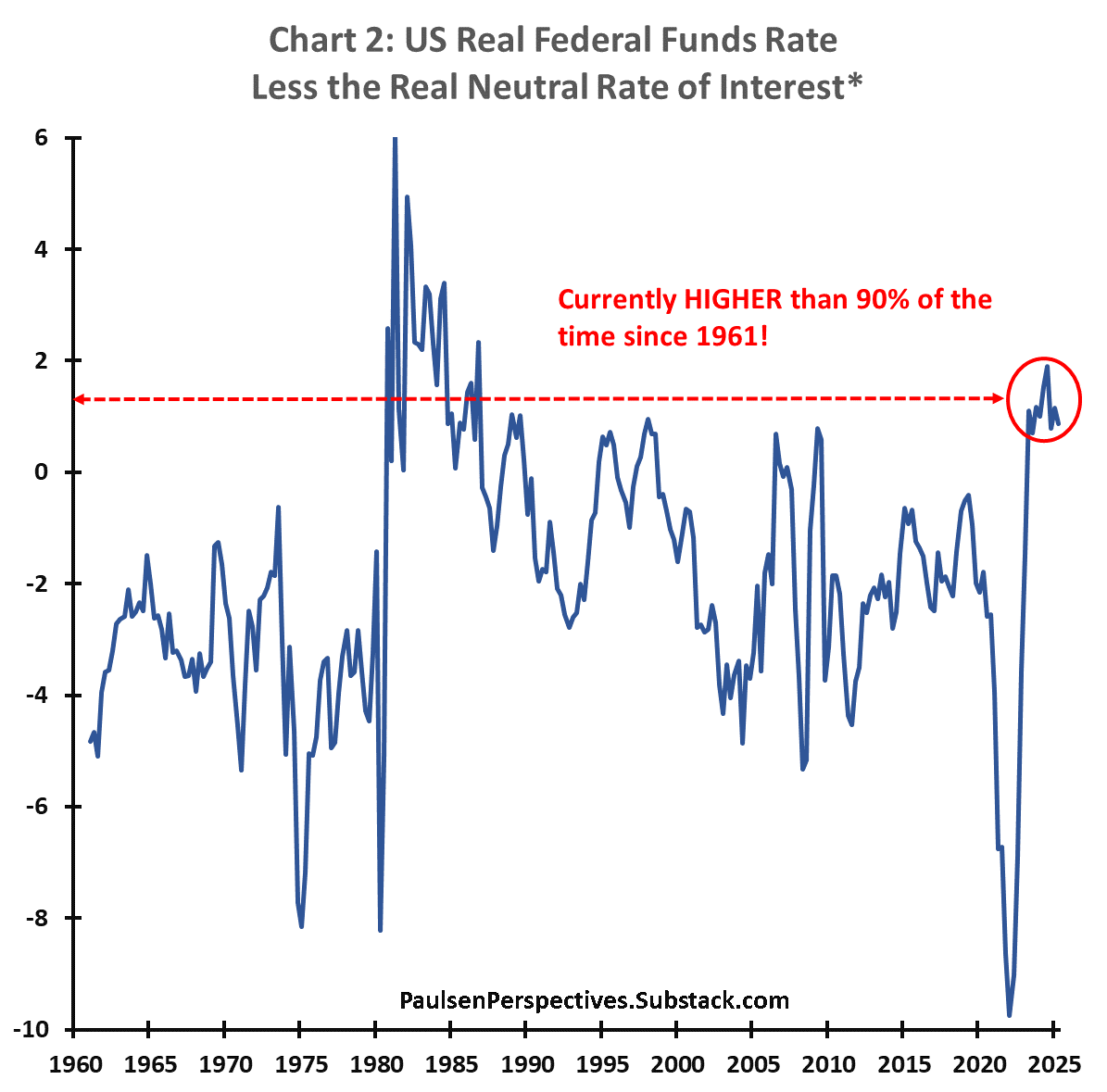

2. The Real Fed Funds Rate is Very High!

The neutral rate of interest, also referred to as the natural rate of interest, is a theoretical short-term real interest rate that maintains the economy at full employment and stable inflation. It is the rate at which monetary policy is considered to be neither stimulatory nor restrictive. As shown in chart 2, the current real Fed Funds rate has been hovering about 1% above the neutral rate during the last couple years which is higher than about 90% of the time since 1961. As shown in chart 2, usually the real funds rate has been below the real neutral rate. Indeed, with the U.S. economy currently growing near 1% in real terms, the situation probably demands a real Funds rate which is 2% or more “below” the neutral rate? The Fed has been and remains much too restrictive.

Keep reading with a 7-day free trial

Subscribe to Paulsen Perspectives to keep reading this post and get 7 days of free access to the full post archives.