A Productivity Story

The link between U.S. innovation cycles and economic performance has changed dramatically since 2000.

Although the Iranian conflict currently captures most of the attention surrounding the financial markets, productivity remains an important story for how this bull market and its corollary economic expansion ultimately ends. A popularized story is that major technological innovations in recent years including artificial intelligence, robotics, and quantum computing have led to explosive productivity gains. Indeed, many believe productivity has become so pronounced that it threatens to create an Orwellian economy with rising real GDP and job losses.

What follows is an examination of U.S. productivity trends since 1998 – mostly since the dotcom bust. During this period, productivity success has primarily been limited to the technology or information sector of the U.S. economy with very little evidence of noticeable gains occurring outside of the center of innovation. Moreover, productivity results even within the information sector have been fairly consistent during the last 25 years – for the most part, despite the introduction of major innovations, productivity gains even in the technology sector have not become noticeably stronger in recent years. Finally, since the dotcom bust, unlike most of U.S. history, productivity results have been mostly limited to periods when overall job creation has been weak. This has been particularly true within the technology sector itself which has suffered severe job losses during the last 25 years. Is U.S. productivity growth since the dotcom era less phenomenal than most appreciate and perhaps primarily the result of a façade tied to weak employment results?

Productivity – Information Sector vs. Rest of the Economy

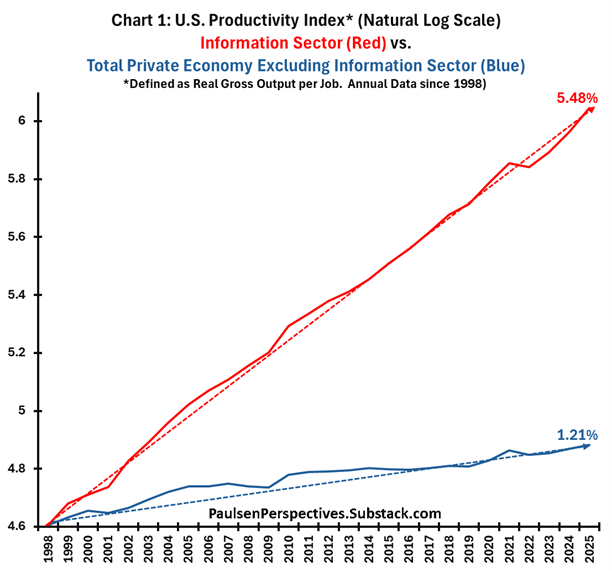

Chart 1 illustrates productivity indexes on an annual basis since 1998 for the information sector (i.e., a proxy for the technology sector) compared to the rest of the economy. Conventionally, productivity is measured as real output per hour of all persons worked. For the purposes of this study and because of limited data availability, productivity is defined as private real gross output per job. While there are differences between these two measures, they are both decent proxies of productivity.

Since the dotcom bust in the late 1990s, U.S. productivity gains have primarily been limited to the center of innovation, the technology sector itself. During the 27 years since 1998, information sector productivity has risen at an average annualized pace of 5.48% compared to only 1.21% in the “rest” of the economy. Chart 1 is shown on a natural log scale and as the dotted lines suggest, the pace of productivity gains both within the information sector and across the rest of the economy have been fairly consistent during this period. Overall, since 1998, information sector productivity has risen by 322% compared to only a 32% gain in productivity outside of the information sector!

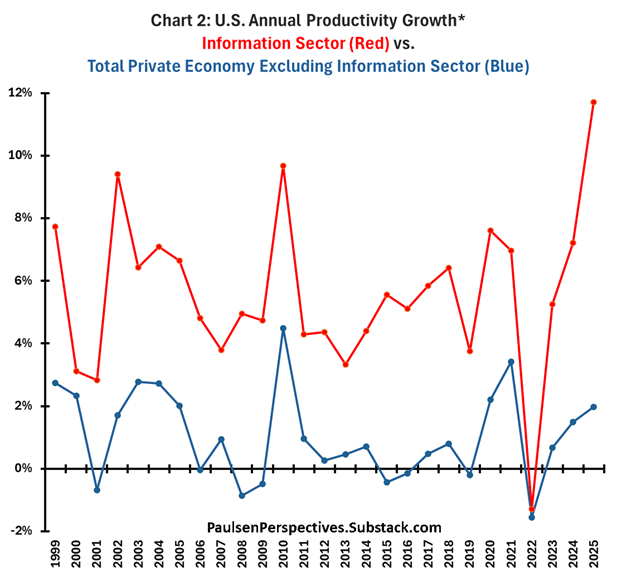

Chart 2 shows the annual percent changes in productivity between the information sector and the rest of the economy. Since 1998, annual productivity within the technology sector has consistently hovered about 5% while growth in the rest of the economy has remained tethered to about 1%. That is, what are widely considered to be dramatic life-changing innovations in recent years – although they have kept technology productivity relatively strong near 5% -- have done little to improve productivity outside of the technology sector. Since the dotcom era, innovation transference has simply not occurred.

Moreover, the cyclical ups and downs of annual productivity seem mostly tied to annual employment growth. As shown on chart 2, since the dotcom bust, annual productivity gains spiked noticeably higher in 2002-03, 2010, 2020-21, and again in 2025. Each of these periods were either recessions (2002-03, 2010, 2020-21) or periods when annual job growth slowed significantly (2025). That is, excitement about annual productivity gains may be misplaced since they seem to be a product of weak economic conditions rather than sustained productivity success. For example, should investors take comfort in the fact that information sector productivity rose by almost 12% in 2025 while productivity in the rest of the economy reached almost 2%? Probably not, since these gains arose when information sector employment “declined” by 1.8% last year and when job growth in the rest of the economy was essentially zero. It’s easy to boost measured productivity in the short run by simply cutting staffs and costs.

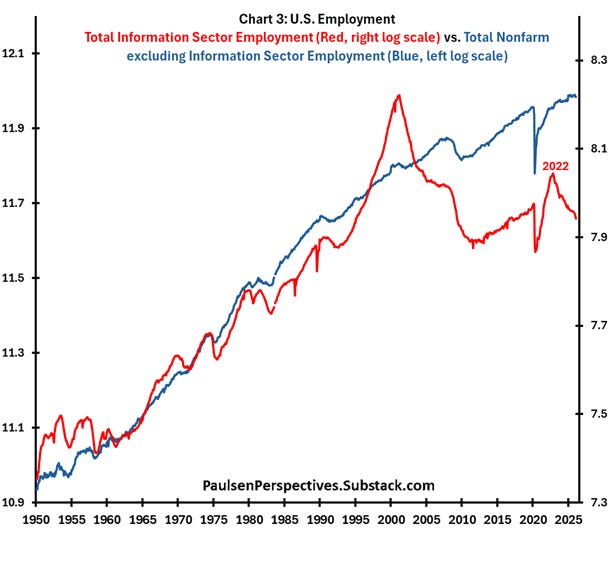

Chart 3 highlights that most productivity improvements since 2000 may simply reflect weaker U.S. employment rather than representing an actual sustained improvement in productivity. This chart overlays employment in the information sector (red line) with employment in the rest of the economy (blue line). They are illustrated on a natural log scale which shows that until 2000, employment growth in both the information sector and the rest of the economy sustained at a stronger pace than since 2000. Since the dotcom peak, job creation outside of the information sector has been noticeably slower and information sector employment has significantly contracted. Indeed, it’s no coincidence the single year that information sector productivity contracted was in 2022 (see chart 2) when job creation in information sector soared. It could be that productivity gains are causing employment growth to slow, but it appears more likely that slower employment growth has been artificially boosting productivity results. More on this later.

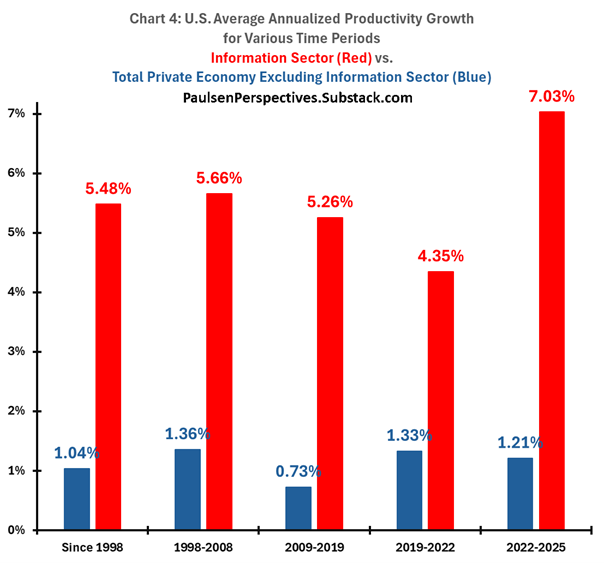

Chart 4 highlights productivity performances for selected periods since 1998. First, it’s clear that productivity results have been very consistent since the dotcom bust. Productivity in the information sector has been persistently strong whereas productivity elsewhere has been consistently underwhelming. No evidence yet showing that major innovations achieved during the last couple decades are successfully and sustainably boosting productivity outside of the information sector. Moreover, the rise in information sector productivity since 2022 may be artificially elevated because this sector has experienced substantial job losses during this time. From chart 3, since the end of 2022, during this official non-recessionary period, information sector jobs have declined at a 2.8% annualized pace! This could suggest the information sector has truly become Orwellian by raising output while persistently cutting jobs, or it could simply represent an artificial boost to productivity which often temporarily rises when job growth slows.

Historical View of Productivity & Job Creation

The relationship between job creation and productivity growth has changed significantly since 2000 and couldn’t be more different from what it was during the 1990s boom or during most of the post-war era.

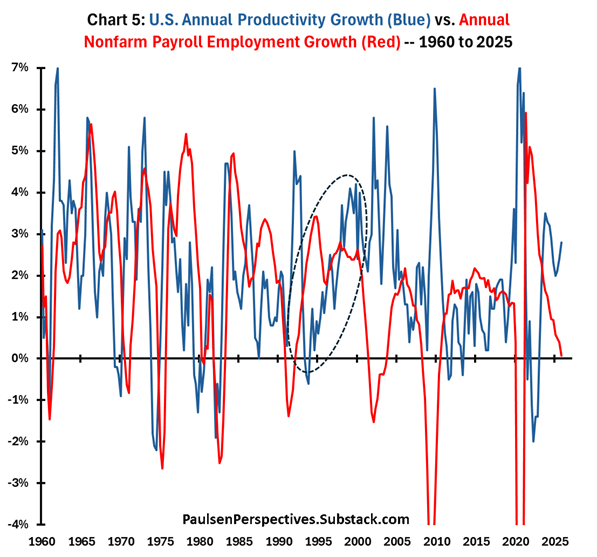

Chart 5 compares the annual growth in U.S. productivity (blue) with the annual growth in nonfarm payroll employment (red) since 1960. Between 1960 to 1990, productivity and employment moved hand in hand. Periods of stronger productivity growth were usually associated with strong employment gains. There was only “good” about productivity – when it rose it not only implied each worker was producing more but it also coincided with companies boosting staffs at a healthy pace. Likewise, when productivity weakened so did employment opportunities. This is the way the post-war economy worked up until at least 1990 and really until 2000.

Note on chart 5 that in 1990, in a fashion very different from earlier in the post-war era, productivity growth surged to almost 5% during a recession which resulted in an annual job loss of almost 1.5%. That is, for the first time since at least 1960, productivity rose while jobs were lost. This didn’t last long because the 1990s dotcom boom began in 1992 and that technological boom was very similar to the earlier post-war era. That is, as highlighted by the black dotted oval, between 1992 to 2000, annual job creation rose and remained near a healthy 2.5% pace throughout the rest of the decade while annual productivity growth also surged higher to about 4% by 2000. The 1990s technology boom was one characterized by superior productivity with superior job creation – a character similar to most of the post-war era between 1960 to 1990.

However, since the dotcom collapse, the relationship between productivity and jobs growth has been turned on its head. In the first half of the 2000s, productivity surged and remained strong while job growth contracted. Then after a brief period when both productivity and job creation hovered between a modest 1% to 2% growth, job growth collapsed while productivity again surged higher during the 2009-2010 crisis. Both productivity growth and job creation were again modest during the 2010 to 2020 expansion and then productivity again surged while job losses mounted during the 2020 pandemic crisis. And when job growth did finally recover in 2021, productivity growth collapsed. Most recently, since 2023 productivity growth has again increased but only while job creation has collapsed to zero.

Many suggest currently productivity is doing well and the U.S. is again experiencing a dotcom-like innovation-led period of renaissance. However, the contemporary environment is nothing like the 1990s nor even anything like U.S. history prior to the 1990s! The correlation between annual productivity growth and annual employment growth from 1960 to 1999 was +0.17 whereas since 2000 the correlation has been -0.70!

For the last 25 years – and very much on display throughout the contemporary bull market – the economy has oddly only enjoyed periods of strength in productivity during periods when job growth has collapsed. And whenever job creation has improved, productivity growth has faltered. For whatever reasons, probably not yet well understood, productivity gains are no longer associated with rising job opportunities. From 1960 to 2000, periods of innovation meant improved job growth. Since 2000, periods of innovation have been associated with job losses.

I’m not sure who is the chicken and who is the egg. Today, are innovations “causing” job losses or are weak job market conditions leading to “artificial and unsustainable” gains in productivity as companies attempt to right-size staff additions to maintain a reasonable reported level of productivity in an economy which overall is growing much more slowly than it did in earlier decades?

Final Comments

It’s almost impossible to learn about the contemporary innovations of AI, robotics, and quantum computing and not be convinced that U.S. productivity is set to explode. How could these new human understandings not lead to great things? And probably, they ultimately will.

However, during the last 25 years, the link between innovations and economic performance has so far proved disappointing. Unlike most of U.S. history, today’s productivity gains – if there are any actually occurring – only happen at the expense of job losses. Moreover, the dissemination of innovations to other parts of the economy beyond the information sector have so far proved elusive.

Will these issues soon be resolved, allowing recent innovations to be enjoyed throughout the U.S. economy? Or is there something not yet well understood that is keeping the U.S. economy from exhibiting more economic health tied to technological advances? I wish I knew the answer to these questions. But what appears clear is the contemporary innovation cycle is unfolding very differently and much less successfully compared to the dotcom era or any era from WWII to 2000.

Thanks for Taking a Peek! Jimp

Disclosures________________________________________________________________

Please note that stocks are inherently risky. Any stock can lose most of its value at any moment, including any stock I mention here. You should never rely on a single source for investment decisions, including me. I am a retired investment strategist offering opinions and observations on the markets, the economy and companies. You should do your own research and also consult a qualified financial planner and investment advisor before making investment decisions.

This communication has been prepared for your informational purposes only. This material is for illustration and discussion purposes only and are not intended to be, nor should they be construed as financial, legal, tax or investment advice. This material presents information through the date indicated, is only a guide to the author’s current expectations and is subject to revision by the author, though the author is under no obligation to do so. The views expressed herein are solely those of the author. This material should not be construed as a recommendation, or advice or an offer or solicitation with respect to the purchase or sale of any investment. The information in this report is not intended to provide a basis on which you could make an investment decision on any particular security or its issuer.

Certain information has been provided by and/or is based on third party sources and, although such information is believed to be reliable, no representation is made is made with respect to the accuracy, completeness or timeliness of such information. This information may be subject to change without notice. I make no obligation to maintain or update this material based on subsequent information and events or to provide you with any additional or supplemental information or any update to or correction of the information contained herein. Any opinions and assumptions expressed herein are made as of the date of this communication and are subject to change and/or withdrawal without notice. No liability is accepted by the author for any losses that may arise from any use of the information contained herein.

Any financial instruments mentioned herein are speculative in nature and may involve risk to principal and interest. Any prices or levels shown are either historical or purely indicative. This material does not take into account the particular investment objectives or financial circumstances, objectives or needs of any specific investor, and are not intended as recommendations of particular securities, investment products, or other financial products or strategies to particular clients. Securities, investment products, other financial products or strategies discussed herein may not be suitable for all investors. The recipient of this report must make its own independent decisions regarding any securities, investment products or other financial products.